We Don't Just Spend Money, We Feel Money

Most people think they know where their money goes.

They've got a rough idea, rent, groceries, that streaming service or gym membership they forgot to cancel. But when you actually map it out, when you see every dollar accounted for, the numbers tell a different story than the one you've been telling yourself.

I've watched this happen hundreds of times. Someone sits down, gets out their statements, and suddenly realise their "occasional" takeout habit is $600 a month. Or that the gym membership they swore they'd use hasn't been accessed in four months. And what about those "small" purchases, the ones that don't feel like they matter but add up to more than their car payment?

When you don’t have a clear picture of what's coming in, what's going out, and how much debt you're carrying, you're making financial decisions blind. You can't plan for the future when you don't know where you are right now.

But here's where I see most people going wrong and I relate to this so much because I used to be no different.

Once they finally see the numbers, their first instinct is to look at where they can cut back. Spend less. Go without. Deprive themselves of the things they enjoy until life starts feeling pretty negative.

That's why I’ve come to hate the word "budget." It puts you in a restriction mindset from the start. It's all about what you can't have, what you have to give up, what you're doing wrong. No wonder most budgets fail within a few weeks.

Plans Work Better Than Budgets

Creating a plan is different. A plan is intentional. It starts with recognising what you actually value and what you don't. Then figuring out how to direct your money toward what gives you purpose.

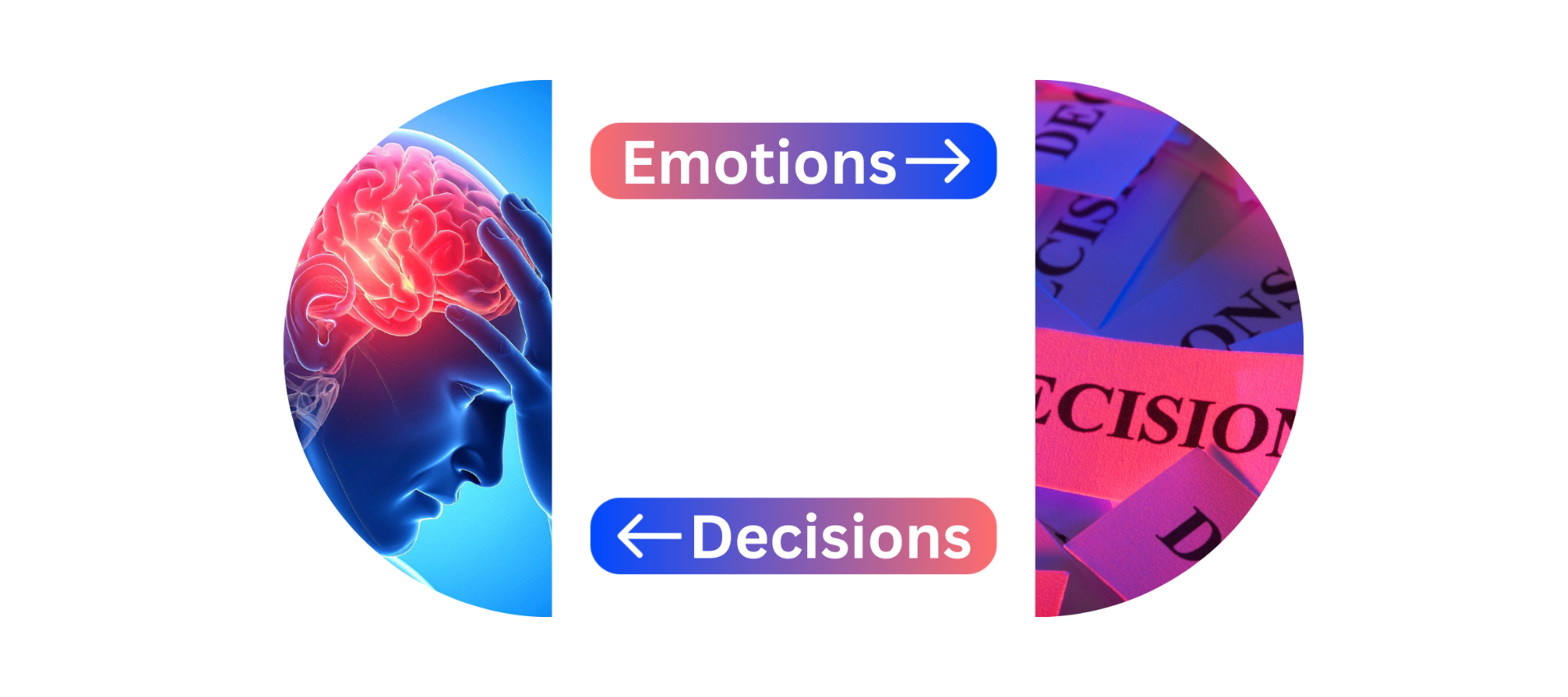

And a plan works better than a budget because of one fundamental reason: we don't just spend money, we feel money.

Stress. Fatigue. Boredom. Pressure. Reward. All of these emotional states drive spending habits. You're not making purely rational decisions with your money. Nobody is. You're making decisions influenced by how you feel in that moment, what's happening in your life, and what spending that money represents to you emotionally.

That $80 you spent at the mall on a Tuesday afternoon? Maybe you were stressed about a work deadline and needed to feel in control of something.

Uber Eats when you have food at home? Maybe you were too exhausted to face another task, and ordering in felt like the only break you'd get all day.

The new course you signed up for at midnight? Maybe you were feeling stuck and buying it felt like taking action, like moving forward, even if you never actually start it.

None of this shows up in a spreadsheet. Your banking app just sees the transaction. But that emotional layer is where your real spending patterns live.

If you're in a relationship, the lack of clear, judgment-free communication around money makes this even harder. You're not just dealing with your own emotional triggers, you're navigating someone else's too.

Sound familiar?

If you're a couple: You probably don't always agree on where the money should go. One of you wants to spend, the other wants to save. One of you sees a purchase as necessary, the other sees it as wasteful. You might have tried talking about money, but it always ends in frustration or avoidance. Sound familiar?

Here's the thing, you're both right. You're just struggling to figure out how to do both. How to save for what matters while also living a life you enjoy now. How to make financial decisions together when you have different values, different triggers, and different ideas about what money means.

If you're single: You're probably still trying to figure out what you really want but without the clarity of defined goals or values, how you feel on any given day or whatever's happening around you socially influences your spending.

You're living money in, money out and maybe you're doing okay. But you know you're not getting ahead either. Your intuition or gut is telling you that you should be doing something different, but you're not sure what.

Either way, you're stuck in a pattern where emotions drive decisions, and decisions create more emotions. You feel stressed about money, so you spend to feel better, which creates more stress, which leads to more reactive spending. And the cycle repeats.

Emotions control your money

I've seen patterns emerge over years of working with clients. The two most common emotions that show up again and again are ‘Guilt’ and ‘Fear’. Behaviours that people can't quite explain when they're looking at the numbers later:

Guilt. You spend on something you "shouldn't," then feel terrible about it. Or you don't spend on something, and feel guilty about that too, guilty that you're depriving your kids, your partner, yourself.

Fear. Fear of not having enough. Fear of missing out. Fear of making the wrong decision. Fear keeps you reactive instead of intentional.

These emotions don't show up in your transaction history. But they're there in every purchase, every financial decision, every money conversation you avoid having.

Obligation, blame and resentment are the other three but we can talk about those another day.

How you can reign in your emotions

Regular, calm money check-ins change things.

Not heated arguments about who spent what. Not avoidance until something breaks. Calm, consistent conversations where you look at the numbers together and talk about what they mean.

Shared goals change things.

When you and your partner (or if you're single, your accountability partner) actually agree on what you're working toward, individual purchases stop feeling like personal attacks or failures.

Understanding your financial values and triggers changes things.

When you know that you spend when you're stressed, or that your partner grew up with money anxiety that shapes how they save, you stop judging the behaviour and start looking at what's underneath it.

Here's what I've learned working with people who actually make progress:

they stop treating money like a math problem and start treating it like a human problem. They recognize that their spending patterns are telling them something about what they need, what they value, and what's not working in their life.

They move from shame to awareness. From blame to curiosity. From restriction to intention.

Theres a difference between knowing and doing

You might be reading this and recognising yourself. You might see your patterns, understand the emotions driving your decisions, and know intellectually what you need to do differently.

But knowing isn't the same as doing.

I've seen people spend years knowing they need to change something but never actually changing it. Because changing your relationship with money isn't about having more information. It's about having someone who can see what you can't see, ask questions you haven't thought to ask, and help you build something that actually works for how you live.

That's what coaching does that spreadsheets can't. It addresses the feelings underneath the numbers. It helps you see patterns you're too close to notice. It creates accountability that's firm but not judgmental. It gives you a strategy that's yours, not something prescribed from a book or copied from what worked for someone else.

Because here's the truth: you're not failing at money because you're bad with money. You're stuck because you're trying to solve an emotional problem with a logical solution. You're trying to budget your way out of something that needs a different approach entirely.

And here’s your opportunity

I've watched people completely transform their relationship with money. Not because they suddenly started earning more or because they white-knuckled their way through a restrictive budget.

But because they finally understood what was actually happening with their money and why.

They stopped reacting and started choosing. They stopped avoiding and started engaging. They stopped fighting with their partner about money and started working together. They stopped feeling like they should be further ahead and started making actual progress.

That transformation doesn't happen by reading another article or downloading another app. It happens when you get honest about where you are, clear about where you want to go, and supported by someone who knows how to help you get there.

If you're tired of feeling like you should have this figured out by now and you're done with the cycle of good intentions that don't stick, maybe it's time to try something different.

Book a free 30-minute call. We'll look at where you are, talk about what's not working, and figure out if coaching is right for you.

Book a call and see if this is right for you

No sales pitch. No judgment. Just an honest conversation about what's possible when you stop treating money like numbers and start treating it like the human, emotional thing it actually is.

Because you don't just spend money. You feel it. And once you understand that, everything changes.